First published 12 Jul 2018 for Mancell Financial Group

The ‘active versus passive’ debate in funds management is a guaranteed space filler in the financial media, but it would help the general public if those making the comparisons got their facts straight.

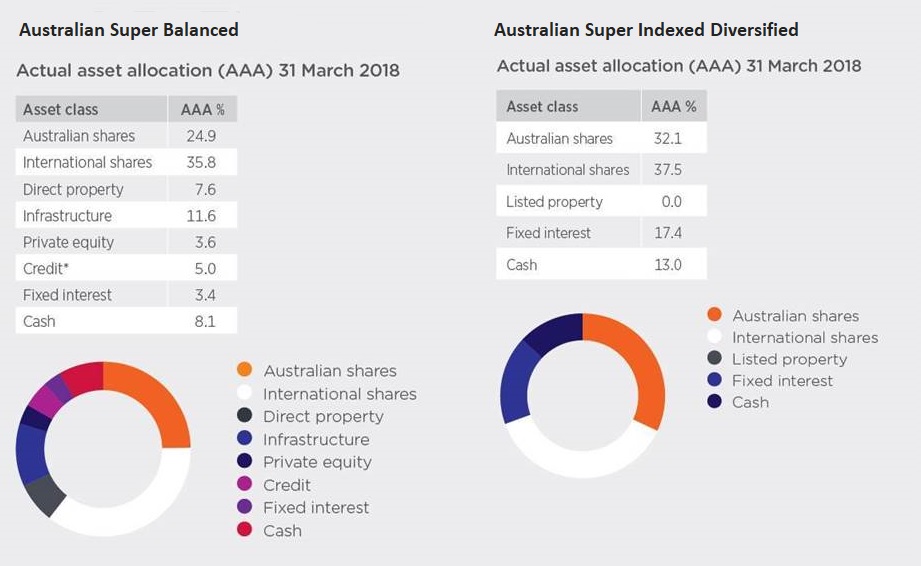

A recent article in Professional Planner by John Peterson of the Peterson Research Institute cited the outperformance of Australian Super’s actively managed balanced option and a passively managed indexed diversified option to justify the argument that actively managed funds do better over time than their passively managed equivalents.

Stop the Press. This is news to us. So we looked in detail at these two vehicles and discovered that while Mr Peterson goes into detail to highlight the similarity between the two. Noting the ‘virtually identical’ investment horizon, risk of negative return and long-term objective, he seems to have ignored one incredibly significant detail.

There’s no allowance for the relative asset allocations of both funds being compared. And if you believe the academics, asset allocation explains around 93.6% of the variation in portfolio returns. With that being the case, it’s a none too small and frankly strange omission.

Bringing up the asset allocation tables from the most recent disclosures available from Australian Super shows it’s not even an apples with oranges comparison. Something closer to apples with potatoes.