A Bronx Tale

Right now is an ugly time. People are out of jobs. Whole societies are cooped up in houses. Minds are wandering. Where does this end? For some, the descent into conspiracy is proving easy. The behaviour of some leaders, government agencies and international organisations hasn’t helped. No wonder people are confused.

In fraught times liquidity is important. Panic leads the mind to many weird and wonderful places. People want certainty. The panicked want cash. The most panicked want cash within arm’s length. Some are talking about making a deposit with the Vegemite jar buried in the garden.

It’s simple. The average person struggles with money. There are two outlooks. Sunshine and lollipops or Buffalo Bill’s basement. Keeping your head in either situation? Good luck. Now? It’s a dark pit with threats of the hose.

I’ve been reminded of this in recent weeks. First it was an email from Vanguard. The sell spreads on some of their managed funds had blown out. A 1.79% clip to exit their corporate fixed interest fund. Woof. The minimum sell for any of their fixed interest products was now .55%. At Vanguard, costs matter, but not if you leave. Sellers won’t be pushing the costs onto those committed to the fund.

The sell spread increase suggests some heavy selling. Corporate bonds during an economic freeze? To be expected.

Keep sliding down the credit pole and this is more likely to occur. Cash is in demand for all manner of reasons. Panicked people want money. No job. Fear. Previous bad decisions coming home to roost. The Vanguard example should serve as a warning. Not for Vanguard, or any other large manager, but the ones seen advertising in the newspaper. Real estate and mortgage funds as a lure for the yield starved. The least liquid people will be under the most stress. This will put stress on the least liquid funds.

Confined in one of those ‘like fixed interest’ funds or ‘better than bank interest’ products? These products are all sunshine and lollipops in good times. In bad times, the manager might just lock the door because there’s a run on the fund. They don’t have the liquidity for your redemption. How many mortgages are on pause right now. How many will fall into delinquency?

There will be ashen-faced investors on current affair programs at the end of this. Some non-advised. Some advised. For the non-advised, it’s the sunshine and lollipops again before getting the hose. A freeze would never be expected. For the advised, the decision was in someone else’s hands. They can rightly ask why and demand answers. Their adviser didn’t do their job.

Equity markets don’t come without declines. It’s the price paid for higher returns. One part of a portfolio is meant to hold up. Defensive. Not getting the yield you expect or think you deserve? Tough. Don’t reach. Fixed interest or bonds shouldn’t be outsourced to mortgage funds, hybrids or some illiquid concoction of foolishness brewed in good times without enough concern for the bad.

Advisers who have tipped clients into this stuff will have some explaining to do. They didn’t use evidence. Advisers with an evidence based process have expectations around the quality of the funds they use. Dubious replacements for fixed interest won’t sneak in. They won’t pass scrutiny. Liquidity should be available when it matters.

Related themes.

Superannuation funds are in a flap. Some hold substantial unlisted assets. Can’t be liquidated quickly. Looks great in good times and keeps their returns looking better in bad times. The government just rocked their boat. Anyone in dire straits right now can withdraw $10,000 this financial year and next. Unexpected and there are implications.

Liquidity concerns have mounted as funds deal with extreme market volatility and suppressed inflows while unemployment climbs amid the total shut-down of some industries.

Unlisted assets, which are harder to liquidate, are also a concern. Two leading industry funds, Unisuper and AustralianSuper, slashed the value of these investments last week by between 6 and 10 per cent. The $44 billion hospitality fund, Hostplus, also has billions invested in unlisted property and infrastructure with major stakes in airports, retail and commercial property.

Superfunds are now begging the RBA for liquidity for the redemptions. While this is without precedence there’s been constant hubris from some funds. No cash, no fixed interest. Getting deeper into private equity and venture capital. The current government is hostile along with associated ideological think tanks. One couldn’t help wonder were they tempting fate. If anyone should expect legislative risk, it’s the superannuation industry.

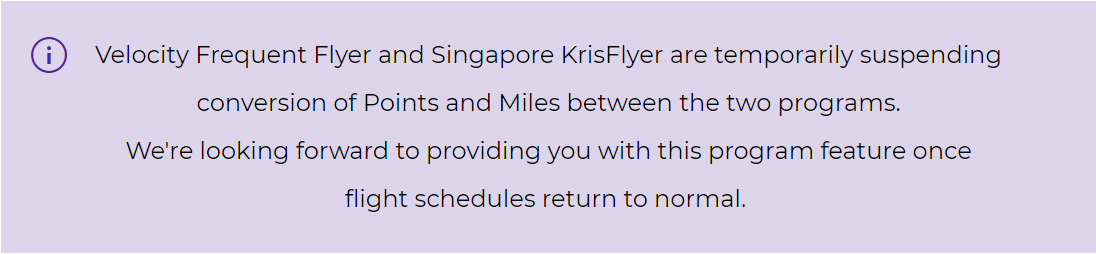

Airlines. Few are flying short term. Even fewer will be flying long term. One of the most precarious, Virgin Australia, has been lobbying the government for a loan. The sharpest knew what the COVID-19 situation meant for Virgin. Velocity points in danger. With an option to transfer to Singapore’s Krisflyer program, the outflow started.

Until a few days ago.

Now youse can’t leave.

Now youse can’t leave.

This represents general information only. Before making any financial or investment decisions, I suggest you consult a financial planner to take into account your personal investment objectives, financial situation and individual needs. Don’t make financial or investment decisions on the basis of blog post or sourcing advice from internet forums, if you’d like a introduction to investing, please consider reading Your Investment Philosophy, which offers an evidence based primer for building your own investment philosophy.